Debt Avalanche Method Calculator Free Google Sheets Worksheet

Get the free Debt Avalanche spreadsheet to run a simulation of the debt avalanche method applied to your debts. There is no need to download any software; the only requirement is a Google account, since the spreadsheet works with Google Drive.

How to use the Spreadsheet?

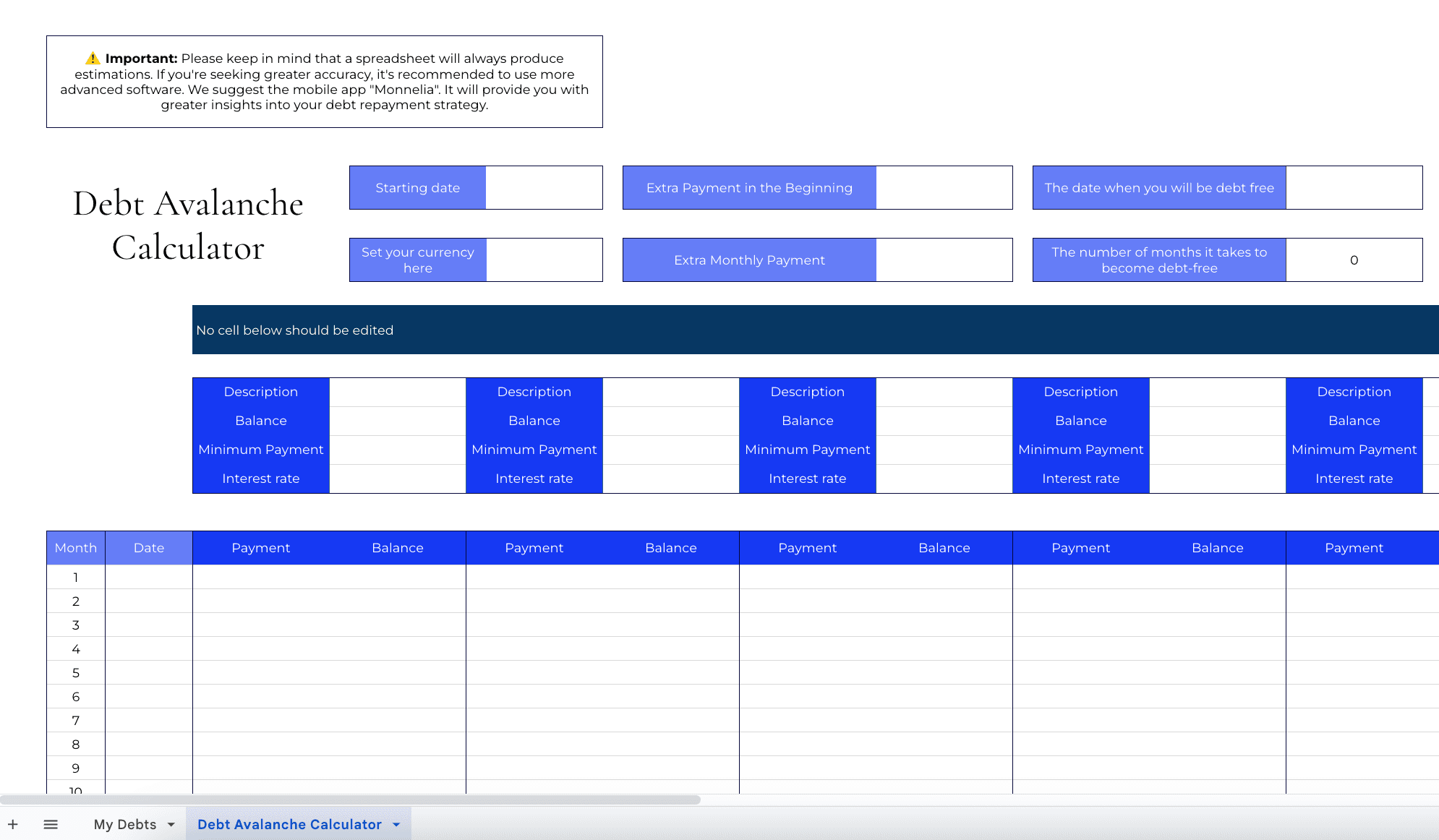

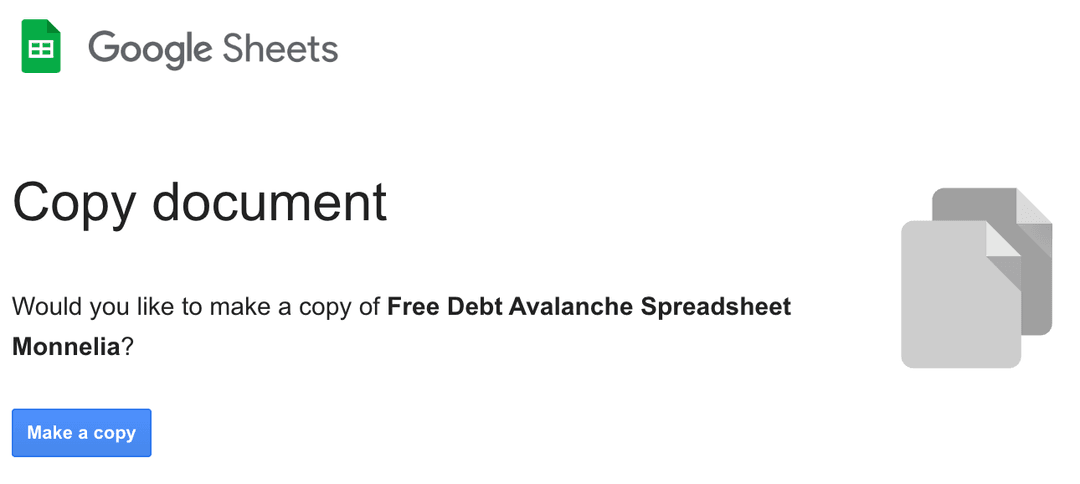

Click on the button 'Access template' above. You will be redirected to a page where you can copy the spreadsheet into your Google Drive. To use this template, you don’t need any software; the only requirement is to be logged into your Google account. If you are not logged in yet, it may ask you to log in. Once you are logged in, you should be asked to make a copy of the spreadsheet in your Google Drive. Click on 'Make a copy'. Every time you need to go back to the spreadsheet, go to Google Sheets and access it from there.

The file contains two tabs: one named 'My debts' to list all your debts, and the other named 'Debt Avalanche Calculator' to see how the debt avalanche method will perform in your situation. In the spreadsheet, most of the cells fill in automatically. In the 'Debt Avalanche Calculator', please make sure not to edit cells X4 and X6.

How to use the Payoff Template with Excel?

If you are more comfortable with Excel than Google Sheets, you can still use the template with Excel. To do this, you need to download the spreadsheet in the xlsx format. First, copy the spreadsheet to your Google Drive following the instructions above. Once this is done, open the template in your browser and navigate to 'File' > 'Download' > 'Microsoft Excel (.xlsx)'. The file should appear in your downloads, and you can now use the spreadsheet with Excel.

What’s the Debt Avalanche method?

The debt avalanche method is a popular strategy for paying off debts more quickly and with less interest. This approach is based on mathematics: you always focus on the debt with the highest interest rate first to prevent interest from compounding. Each time the debt with the highest interest rate is paid off, you roll its minimum payment over to the next debt with the largest rate. Over time, all the minimum payments accumulate, helping you to repay your debts faster.

Step-by-Step Process for Successfully Implementing the Avalanche Method

Applying the avalanche method to your situation is every easy, here is a step-by-step process to guide you through the process.

Step 1: Write Down Your Debts

List all your debts, including balances, minimum payments, and interest rates.

Step 2: Order Debts by Interest Rate

Sort your debts in descending order based on the interest rate, beginning with the highest interest rate first.

Step 3: Continue Making Minimum Payments

You still have to continue making the minimum payments on all your debts to avoid any penalties. You should not put any extra money towards debts that are not top priority (i.e., debts with a lower interest rate), make only the minimum payment required for these debts.

(Optional) Step 4: Allocate Extra Funds to the Highest Interest Debt

If you can afford to put extra money towards debt repayment each month, use this extra amount to repay the debt with the highest interest rate on your list. This step is optional but can be a game-changer since it will save you a lot of money on interest in the long run and make you debt-free much faster.

Step 5: Pay Off the Highest Interest Debt

Continue paying the minimum payment plus the extra amount until the debt with the highest interest rate is completely paid off.

Step 6: Move to the Next Highest Interest Debt

Once the highest interest debt is paid off, take the total payment amount you were making on that debt (the minimum payment plus any extra amount) and add it to the minimum payment of the next highest interest debt on your list. This step is crucial to benefit from the compounding effect.

Step 7: Repeat the Process

Continue this process of rolling over payments to the next highest interest debt until all debts are paid off!

Download the free Monnelia app to easily keep track of all your debt!

Download MonneliaWhat Are the Benefits of This Method?

This method is typically the most cost-effective, as focusing on repaying the debts with the highest interest rates first prevents interest from accumulating over time. However, this method can sometimes be discouraging if the debt with the highest interest rate also has the largest balance. This debt will take a while to pay off, and you might feel like you’re not making any progress. In this situation, you should stay focused and keep up with the process.

Furthermore, this method works perfectly with all kinds of debts: car loans, house mortgages, student loans, credit cards, etc.

Should I Use the Avalanche or Snowball Method?

Many people are torn between the debt avalanche and snowball methods. The best method depends on your priorities. If you want to save the most money, the avalanche method is likely better. However, the debt snowball method has a significant advantage: it keeps you motivated. Unlike the debt avalanche method, the debt snowball method focuses on repaying the debts with the smallest balance first. With this technique, you will feel like you are making more progress. It’s a 'psychological trick' that incentivizes you to be consistent with your debt repayment.

There is no clear answer to the question of which method is best; it really depends on what you want to achieve.